The coastline at Bagamoyo has a strange kind of energy these days. It’s neither the quiet neglect of an abandoned dream nor the chaos of a construction boom. Instead, it feels like a chessboard before the first move, every piece studied, every possible opening debated, but no one in a hurry to commit.

Here, on these sandy stretches north of Dar es Salaam, Tanzania once planned to build East Africa’s largest port: a deep-sea giant capable of berthing mega-container ships, anchored to a 9,000-hectare special economic zone that would buzz with manufacturing, logistics, and trade.

That vision hasn’t disappeared. But after the 2019 breakdown of the original deal, Bagamoyo has shifted from the fast lane into a careful, deliberate review. The government is now asking a different set of questions: How do you structure a $10 billion project so that it strengthens national trade capacity without locking the country into risky financial terms? How do you attract investors without giving away the store?

In short, how do you build a mega-port the right way, the second time around?

Why a Reboot Is Needed

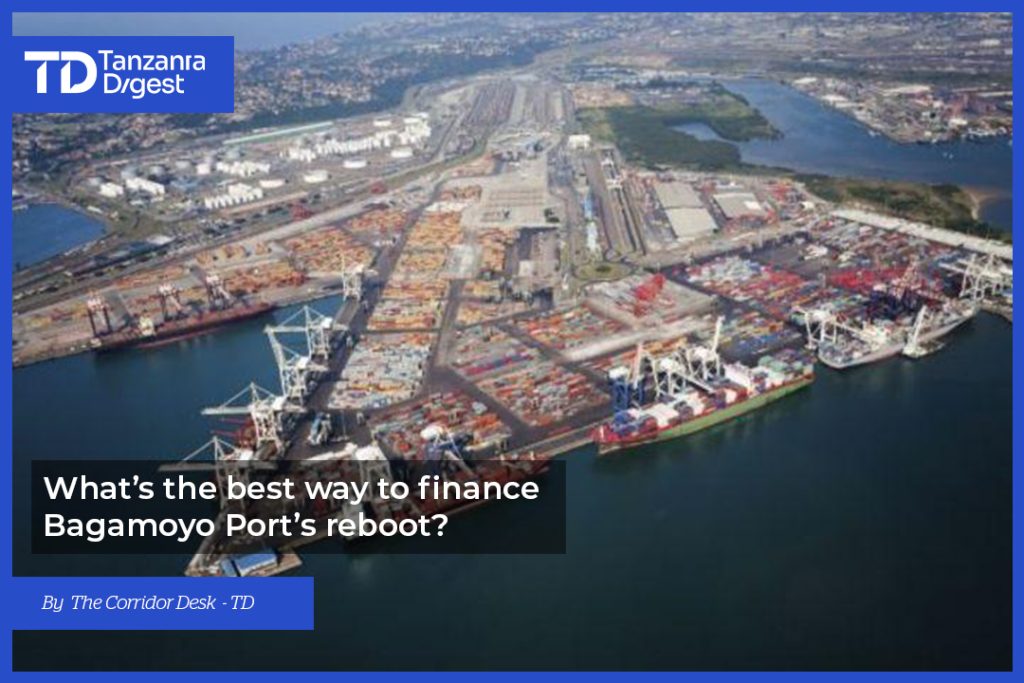

Tanzania’s need for expanded port capacity is not theoretical, it’s arithmetic. Dar es Salaam Port handled about 23 million tonnes in 2022, and projections suggest it could hit 30 million tonnes by 2030 if current growth trends hold. Even with efficiency upgrades, dredging, and terminal automation, Dar will eventually face the limits of its physical footprint.

The pressure is mounting from multiple directions:

- Industrial growth: The Bagamoyo SEZ and other industrial zones are set to generate significant export and import traffic, which will require direct deep-sea access.

- Regional trade integration: The African Continental Free Trade Area (AfCFTA) and East African Community (EAC) market expansion mean more cargo moving across borders.

- Competition: Ports like Mombasa (Kenya), Lamu (Kenya), and Beira (Mozambique) are vying for the same hinterland markets, Uganda, Rwanda, Burundi, eastern DRC, and Zambia.

- Opportunity cost: Every year without progress at Bagamoyo is a year competitors can consolidate their market share.

The government’s own revenue ambitions reflect this urgency. In its 2025/26 targets, the Tanzania Ports Authority (TPA) expects to collect TZS 1.38 trillion in port revenues, an increase driven partly by expanding capacity across the network. Bagamoyo’s eventual contribution could be transformative, but only if it’s built on sustainable terms.

Lessons from the First Attempt

The first iteration of Bagamoyo was born in 2013, under a tripartite agreement between the Government of Tanzania, China Merchants Holdings International (CMHI), and Oman’s State General Reserve Fund (GSRF). On paper, it was a blockbuster: a deep-sea port to rival Mombasa, integrated with Africa’s largest SEZ, promising to handle up to 20 million TEUs annually once complete.

Yet by 2019, the project had collapsed in a very public way. President John Magufuli famously called the proposed terms something “even a drunkard would not accept.” His criticisms boiled down to three key points:

- Sovereignty Risks: The perception that the concession period and operational control clauses gave away too much decision-making power for too long.

- Fiscal Risks: Sweeping tax exemptions and revenue-sharing formulas that, in the government’s view, would yield minimal returns in the early decades.

- Strategic Misalignment: A lack of clarity on how Bagamoyo would fit with Dar es Salaam’s existing role, risking duplication and internal competition.

Some of these points were hotly debated in policy circles. Supporters of the deal argued that the scale required long-term concessions to attract capital; critics countered that sovereignty and flexibility were worth more than speed. What’s clear in hindsight is that the original framework was politically unsustainable, and once the politics turned, the deal had no lifeline.

Financing Models for the New Bagamoyo

If the first Bagamoyo was a bold leap, the second will have to be a carefully engineered bridge. Financing is at the core of this rethink.

Public–Private Partnerships (PPPs)

The most likely model for the reboot is a Build–Operate–Transfer (BOT) or joint-venture PPP. These would allow private investors to fund and operate parts of the port for a set period before handing it back to the state. The difference this time is likely to be shorter concession terms, linked to performance milestones.

Blended Finance

Instead of relying heavily on a single investor or lender, the government could combine sources: private capital, concessional loans from development banks, and climate or infrastructure funds. This spreads risk and increases negotiating leverage.

Phased Funding

One lesson from Morocco’s Tangier Med and South Africa’s Ngqura is the value of phased expansion. Instead of building for full capacity upfront, Bagamoyo could start with a smaller number of berths and scale up as cargo volumes grow. The TPA’s TZS 22 billion allocation in FY 2024/25 for preparatory works is a nod to this approach, keep the project moving in smaller, manageable steps.

Comparative Lessons

- Tangier Med (Morocco): Started small, grew into a mega-hub with consistent governance and investor trust.

- Hambantota (Sri Lanka): Overbuilt early, struggled with debt, eventually leased to a foreign operator for 99 years, a cautionary tale Tanzania is keen to avoid.

The financing model chosen will ultimately define Bagamoyo’s power balance: who takes the risks, who reaps the rewards, and how flexible the country will be in adapting the port’s role over time.

Structuring for Investor Confidence & Public Protection

The balancing act for Bagamoyo’s reboot is clear: make the project attractive enough to draw serious investors, but structure it tightly enough to safeguard Tanzania’s fiscal and strategic interests. That requires more than a good pitch deck, it needs governance embedded in the contract from day one.

Shorter Concession Periods with KPIs

Instead of multi-decade lock-ins that tie the government’s hands for generations, the concession period could be segmented into shorter blocks linked to performance benchmarks. Meet the milestones? The concession extends. Fall short? The state can retender or restructure.

Tariff Transparency and Regulation

Investors need predictable revenue models; the public needs protection from monopolistic pricing. A transparent tariff framework, reviewed periodically by an independent regulator, can protect competitiveness while allowing a fair return for operators.

Dispute Resolution and Renegotiation Clauses

One of the silent killers of mega-projects is the absence of clear, neutral dispute-resolution pathways. Embedding arbitration mechanisms and periodic renegotiation windows can prevent small disagreements from spiraling into years-long stalemates.

Independent Oversight

An independent Bagamoyo Oversight Board, with members from government, industry, and civil society, could monitor compliance on finance, operations, and environmental safeguards. Public quarterly reports would go a long way toward building both investor and citizen trust.

This level of structural foresight does more than manage risk, it signals to the market that Tanzania is a disciplined infrastructure partner, making it easier to secure financing on better terms in the future.

Integrating Bagamoyo into a National Port Strategy

Perhaps the most important question in Bagamoyo’s reboot is not how to build it, but where it fits.

Dar es Salaam’s Modernization

Dar is not standing still. With the Adani Group now operating Container Terminal 2, plus dredging, berth extensions, and digital customs reforms underway, Dar is positioning itself as a faster, more efficient hub. That makes Bagamoyo’s role in the national system even more critical to define.

Cargo Segmentation

One viable approach is to designate Bagamoyo as the primary port for mega-container vessels and high-volume transshipment, while Dar focuses on mixed cargo, bulk goods, and feeder services to smaller regional ports. This mirrors Morocco’s Casablanca–Tangier Med arrangement, where each port serves a distinct niche to avoid cannibalization.

Corridor Integration

Bagamoyo’s competitive edge will hinge on how well it’s tied into the country’s transport corridors. That means synchronizing port construction with Standard Gauge Railway (SGR) phases, trunk road upgrades, and logistics hubs along the Central and Northern Corridors. Without these links, Bagamoyo risks being a “big port in the wrong place”, impressive in capacity but hamstrung by bottlenecks inland.

The SEZ Linkage

Bagamoyo’s 9,000-hectare Special Economic Zone is not an optional extra, it’s the port’s natural demand engine. The SEZ’s planned factories, processing plants, and warehouses could generate year-round cargo flows, reducing the port’s reliance on unpredictable transshipment markets.

Early-Phase Industries

Even before the port’s berths are operational, early industries in the SEZ could begin production, using Dar es Salaam for exports while Bagamoyo readies its docks. This would create a seamless transition once the port is live.

Synchronizing Timelines

One of the first deal-design missteps was the lack of coordination between port and SEZ development. This time, the timelines should be integrated, roads, power supply, and water infrastructure for the SEZ should be ready in tandem with the first port phase.

Incentives and Policy Levers

To attract early SEZ tenants, the government could offer targeted incentives, not blanket tax holidays, but sector-specific perks tied to job creation, export performance, or technology transfer. This keeps benefits measurable and aligned with national goals.

A thriving SEZ will not only justify the port’s existence but also ensure that Tanzania captures the full value chain, from manufacturing to maritime logistics, instead of being just another transit point for foreign-owned goods.

Global & Regional Comparisons

Bagamoyo’s reboot is not happening in a vacuum. Around the world, and especially across Africa, there are instructive examples of what to do and what to avoid in building mega-ports.

Tangier Med, Morocco

Launched in 2007, Tangier Med began with a modest initial phase and clear governance structures. It expanded in stages based on actual cargo growth, eventually becoming the largest port in the Mediterranean. Transparent tariffs, strong corridor connectivity, and an integrated industrial zone were central to its success.

Ngqura, South Africa

Developed alongside Port Elizabeth, Ngqura was positioned as a niche deep-water container port. By avoiding direct competition with its neighbour and aligning operations with broader national logistics strategies, it carved out a profitable role.

Hambantota, Sri Lanka

A cautionary tale. Overbuilt from the start, Hambantota failed to attract enough cargo, leading to financial distress and a controversial 99-year lease to a foreign operator. The lesson for Tanzania is clear: scale must match realistic demand projections, and sovereignty safeguards should be baked in from the outset.

Lamu, Kenya

Part of the LAPSSET corridor, Lamu’s deep-sea port has struggled to secure significant cargo volumes despite its modern infrastructure. Weak hinterland connectivity and an underdeveloped industrial base highlight the importance of aligning port development with inland logistics and local economic activity, exactly the integration Bagamoyo must get right.

Policy Checklist for a Reboot

For Bagamoyo to become a cornerstone of Tanzania’s maritime future rather than another stalled ambition, the following should be non-negotiable:

- Governance Reform & Transparency

- Public disclosure of contracts, tariffs, and performance data.

- Independent oversight body with cross-sector representation.

- Flexible Financing & Concession Terms

- Phased development tied to demand growth.

- Shorter concessions linked to KPIs, with built-in renegotiation points.

- Environmental & Social Safeguards

- Comprehensive Environmental and Social Impact Assessments (ESIAs) before each phase.

- Community benefit-sharing mechanisms for affected areas.

- Integration with Trade & Transport Corridors

- Full coordination with SGR timelines, trunk road upgrades, and logistics hubs.

- Streamlined customs processes aligned with AfCFTA and EAC facilitation agreements.

- SEZ Synchronization

- Industrial tenants confirmed and operational in sync with port commissioning.

- Incentives tied to job creation, export value, and technology transfer.

Building It Right This Time

Bagamoyo is getting its second chance, and with it comes the opportunity to turn a once-stalled project into a model for how Africa builds large-scale infrastructure in the 21st century.

The urgency is real: regional competitors are racing to secure cargo flows, and Dar es Salaam’s capacity crunch is only a matter of time. But this time, the goal is not speed; it’s structure.

A successful Bagamoyo reboot will be one where the financing is balanced, the governance is transparent, the port’s role is strategically defined, and its industrial hinterland is primed for action from day one. If Tanzania gets those elements right, Bagamoyo could emerge not just as another port, but as a genuine economic engine, one that drives growth, anchors trade, and safeguards sovereignty for decades to come.

The coastline is ready. The question now is whether Tanzania’s next move will finally bring Bagamoyo from the drawing board to the shipping lanes, and do so on terms the country can be proud of.

hiI like your writing so much share we be in contact more approximately your article on AOL I need a specialist in this area to resolve my problem Maybe that is you Looking ahead to see you